BestCashCow released updated bank and credit union financial information with the latest data available from the FDIC and the NCUA. Using this information, the site has calculated key financial ratios for every bank and credit union in the United States. For banks, this data includes:

- Texas Ratio - a measure of a bank's ability to weather loan losses.

- Return on Equity

- Capitalization

- Ratio, Asset, Deposit, and Loan trends for the past give years.

For credit unions, the data includes:

- Texas Ratio

- Net Worth - Ratio that measures how much total assets exceed total liabilities.

We provide this information to so that you can understand the financial condition of the institutions you bank with, or are thinking of banking with. While every bank on BestCashCow is FDIC insured and almost every credit union is NCUA insured, there are downsides to banking with a distressed bank or credit union. These include:

- A deterioration of customer service as cost cutting becomes more of a priority.

- The potential to lose interest on CDs. When a bank is taken over, it does not have to honor rates on CDs.

- Lower rates. BestCashCow research has shown that banks in stronger financial condition tend to offer better rates. Banks in worse financial condition do the opposite.

- Bailouts. Ultimately, the general public bears the cost of supporting and propping up distressed financial institutions

As an example, this link shows a financial snapshot of JP Morgan Chase Bank, the largest bank by assets according to BestCashCow.

View the financial condition of any bank.

View the financial condition of any credit union.

Trends in Bank Data

Not only has every bank and credit union been updated, but we spent some time crunching through the numbers at a high level to see what is going on in the banking world. In general, the data shows a banking industry that is awash in cash, not lending, and slowly mending.

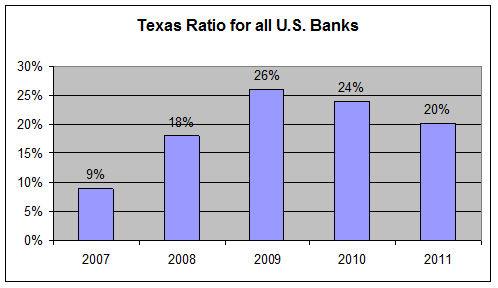

The first chart shows that the Texas Ratio for all U.S. banks has continued to decline after peaking in 2009.

The Texas Ratio measures bank stress and stability with a number over 100% indicating that a bank cannot cover all of its potential losses. The lower the number the better. The chart shows that the ratio spiked in 2008, went higher in 2009 and has been gradually coming down since then. The banking sector is healing. (Read more about how the Texas Ratio predicts bank failure.)

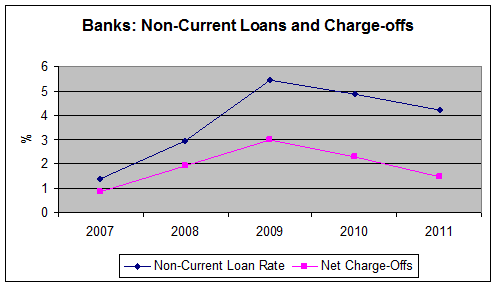

I then examined two main components of the Texas Ratio, non-performing loans and bank capitalization. Non-performing loans peaked in 2009 and have been coming down over the past two years. This indicates that not as many loans are going bad, a good sign for bank health.

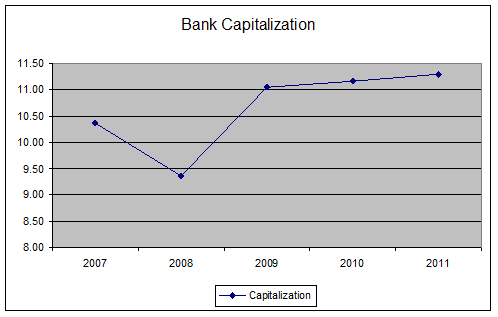

Capitalization dropped in 2008 and then has gradually been increasing. Banks have raised money both from the government (via TARP) and from private investors to bolster their capital. Both an improvement in loan losses and in bank capitalization have contributed to an improving national Texas Ratio.

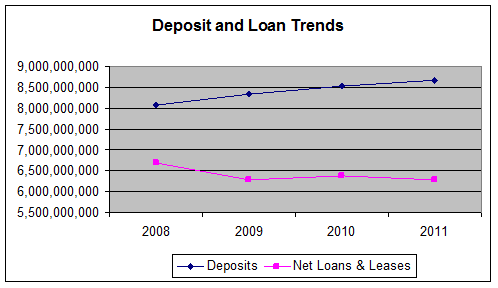

Over the last four years, bank deposits have grown from $8 trillion in 2008 to $9 trillion today. Individuals and corporations are parking their money in cash. Demand for cash is not high which is one reason banks have been able to drop savings and CD rates to record lows. Many banks simply don't need your money and have more cash than they know what to do with. We have heard anecdotally of some banks locking in cash at low rates now in anticipation of a rising rate environment over the next couple of years. Notice though that loan growth has not kept pace. Bank loans have dropped from $6.6 trillion in 2008 to $6.3 trillion today.

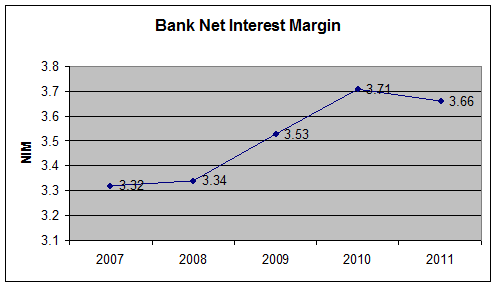

What are banks doing with that extra money? Investing it, most likely in US Treasuries and other safe investments. The next chart shows what has happened to bank net interest margin. Net interest margin is the difference between the rate banks pay depositors for their cash, and interest rate they lend the money. That difference is income for the bank.

Notice the increase starting in 2007 as the Fed lowered short term rates and banks lowered deposit rates. NIM increased until 2010 and has begun to come down. That's not because deposit rates have gone up, but because rates on bonds and Treasuries have dropped, squeezing the banks profit. Eventually if this squeeze continues, banks will be forced to deploy their deposits in a more profitable way. That's good news for those looking for loans to finance a business, house purchase, or a car.

In addition to tracking the financial condition of every bank and credit union, BestCashCow also tracks CD and Savings rates for thousands of banks and credit unions. To see the rates and financial conditions of a bank in your area, view our local bank finder.

Have any questions or comments? Post them below.

Comments

Henry Rice

December 22, 2011

Thanks for the info! Do you think banks will start lending more in 2012?

Is this review helpful? Yes:0 / No: 0

Sol

December 22, 2011

@Henry Rice

Yes, I think lending will increase in 2012. Banks are sitting on a lot of cash and as their balance sheets continue to improve will be willing to take more risks. If interest rates head up that will also serve as an impetus to start lending.

Here's an article with one data point about increased lending:

http://finance.yahoo.com/news/banks-not-lending-corporate-borrowing-181012870.html

Is this review helpful? Yes:0 / No: 0

Add your Comment

use your Google account

or use your BestCashCow account